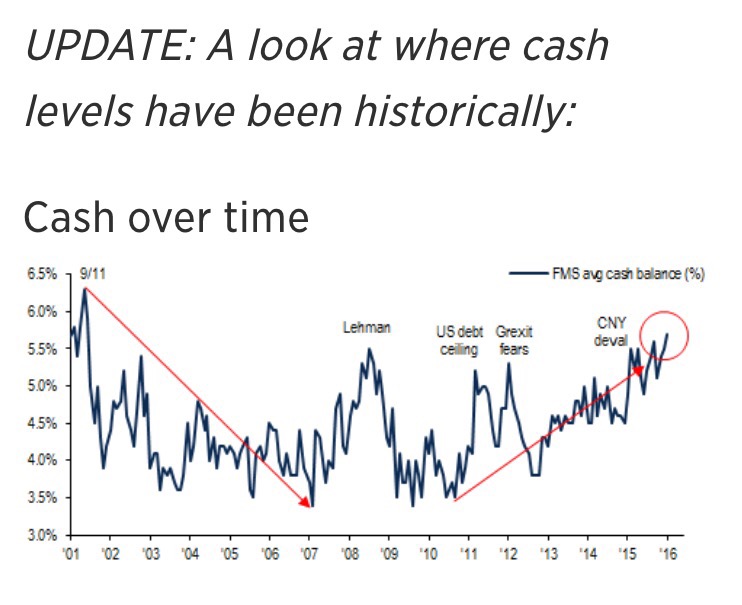

I found this chart to be kind of comical in the sense that it signifies almost nothing. Yet, it’s been cited by a big bank and it’s hit the CNBC newsfeed. Could a 2.5% swing in the level of current cash holdings in mutual funds mean all that much? Seems like an insignificant squiggly line to me.